What’s the deal with that?

Ha!

.

I’m hoping this is the motivation which forces all those stupid yuppie “Change” voters to realize what a dry up the rear screwing their far left liberal views caused once their insurance plans are dropped.

While my employer also covers all health care costs, I am fully aware that it will cost me and every American plenty. No free lunch.

Employers who pick up the cost will now have overhead burden employee. That will i crease cost and force prices of goods and services higher. Likely will result in not being able to keep on as many workers long term or not hire as many new ones as they planned; that is, fewer jobs and higher prices overall.

Also it is sure to degrade medical care since govt has even more control, such as the notorious death panels. You will not be able to buy your Cadillac policy without a hefty fine and the govt will be the one rationing care.

Nobody will come out of this as good or better off except the exempted politicians, govt employees, and fascist crony corps who play ball.

There is one group that may come out ahead provided the exchange websites eventually function. That group is the 30 million people who are chronically uninsured/uninsurable. In other words, 300 million will suffer so that 30 million people may have the opportunity for coverage. It remains to be seen how many of those uninsured will take advantage of this opportunity.

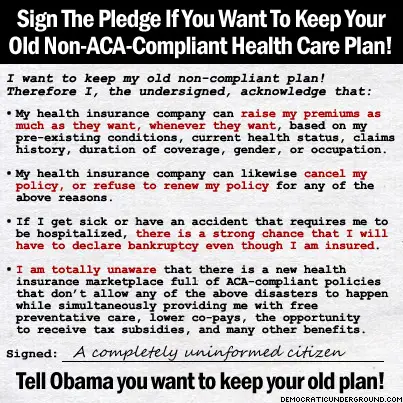

From DU:

^ it pains me to no end to have to acknowledge that those morons are my fellow countrymen.

Sent from my DROID X2

Scary that theyvvote and steer thousands of pounds of steel hurtling down the road at 70 mph! At least most of them are never behind a trigger.

Don’t be negative. The autopsy is free. :dance3:

I now have my new insurance. For me, my insurance rates went up 20+% and co pays went up to boot.

As I mentioned in the past, the national program is based on the MA program, which has been a disaster for MA. I saw my insurance rates sky rocket after the MA plan was added.

I have not used the web page to compare because it continues to be unusable every time I have tried.

Huh? If anything I thought the one thing that ‘worked’ was everyone can get insurance- as everyone’s rates go up.

Am I the only one concerned about the lack of security in the application process, severely exposing one to I.D. theft, plus the so-called navigators aren’t being screened for criminal records? Navigators have been known to give out incorrect information and in some cases suggesting things that’re illegal.

That alone is enough for me not to sign up - never mind the insane increase in deductibles and premiums.

I haven’t had insurance since I left the Army in 2010 and luckily haven’t had any major illnesses or injuries. I’ve paid out of pocket for all my checkups and the occasional Z-pack for a cold bug back in 2011. My wife has since added me to her insurance she gets through her employer and for myself, her, and our son we pay $180 per month. Not bad.

Not the point though. From 2011-2013 I worked for a major outdoor retailer making some decent scratch at 36 hours a week. Not the best hours and not the best pay but I was also a student and was receiving BAH from the post-9/11 GI Bill. It paid the rent and got us macaroni and cheese to live on and I enjoyed the work and time off. Come January 1st of this year employee hours were cut to 25 a week due to the employer mandate (that had not yet gone into effect yet, I blame my employer for that.) I saw my paychecks cut back a third and ended up having to take up a second part time job to make ends meet.

Now I have a new job with a local business that gives me better hours, better pay, and is expanding into a larger facility next year. In this climate it pays to work somewhere that has less than 50 employees.

I have always had a good selection of health insurance where I work.

This year the pay deduction doubled and all of the copays more than doubled. Sounds like a real winning plan to me. My case was not unique, everyone and every available plan from the company had the exact same thing happen.

Wouldn’t even give me a quote. My girlfriend signed up for it, and she went from paying $120, to $300 a month. The quote the site gave her was $140.

I can’t even log into it now. Regarding the Cover Oregon site.

You’re NOT a freeloader for refusing to pay for services which you did not receive.

Actually you don’t have to pay the penalty.

Due to the fact that the only way the “penalty” was constitutional was to declare it a “tax”, the only way they can “take” it from you is to deduct it from your tax refund.

Adjust your withholding allowances so that you get more take home in each check and don’t get a refund or pay a small amount at tax time.

No refund, no penalty.

Nobody should be giving the GOV a free loan all year anyway.

Actually the coffer will just tell you to pay them the money.

That’s funny. I thought the same thing. I’m going to call another company next Monday.

Does the HIPPA law apply to Obamacare?

No - You can’t expect confidentiality with your medical records.

If this doesn’t matter to you, then no problem, but if it does, you’re SOL.

-

Wife’s privately purchased and underwritten insurance being canned due to new rules. Isn’t that awesome? Government can come in to a private contractual arrangement and end the mutually agreed contract. Personally it was best to move from from top-shelf coverage canned by Obamacare at $401/ month to group coverage at $550/month. Didn’t even bother to pull the trigger on taxpayer subsidized insurance through the exchange. What a repulsive experience.

-

Personally involved in process for another Husband/Wife. Was paying $493/month. His coverage is ending 12/31 and wife coverage ends next October due to same unreasonable government power. So both had coverage dumped due to new law. Too bad for them I guess. Under health care exchange, his only option, $949/month. Subsidy is $500 month based on income. So I guess he will be OK for now.

What a crock of garbage this is.